The Reserve Bank of Australia (RBA) recently announced that it would slow down its bond buying efforts given the national economy is in better shape than was previously predicted.

That said, the current lockdown in Sydney may yet slow down their slow down efforts, depending on how protracted that ends up being.

However, the central bank is also confident that the economy will bounce back strongly after the lockdown – just as it has done a number of times over the past year and a half.

Of course, when the Reserve Bank holds a press conference – which is unusual – it means it has something very important to communicate.

The problem is that most of us don’t actually understand what they are communicating a lot of the time, including its most recent one!

Plus, what does any of it have to do with property?

So, to rectify this gap in our collective knowledge bases, I thought I’d pull together some explanatory insights from the Reserve Bank of Australia itself as well as Canstar so we all better understand about the implications of bond buying on property more generally.

What is bond buying anyway?

High levels of government bond buying is another term for quantitative easing (or QE), which is an unconventional monetary policy used in other countries but not in Australia until late last year.

Some people think it involves printing money literally, but it doesn’t.

Rather, it involves central banks buying billions of dollars in government bonds to increase the supply of money to the economy.

According to Canstar, most central banks use their cash reserves to buy government bonds or other financial assets, which starts the process of stimulating a spending cycle.

In essence, it’s like a central bank taking money from its own wallet and buying something from the government or from a regular bank.

This, in turn, provides additional cash that can be used to stimulate the economy via tax cuts or infrastructure spending from the government or via home loans if it’s from banks.

Generally speaking, it also helps to keep interest rates lower for longer because of the increased competition between banks when consumer borrowing activity is strong – like it is now.

Likewise, by purchasing the bonds, the RBA effectively increases demand for them, which leads to a decrease in interest rates for those bonds, according to Canstar.

This then enables the government that initially sold the bonds to borrow money at lower rates.

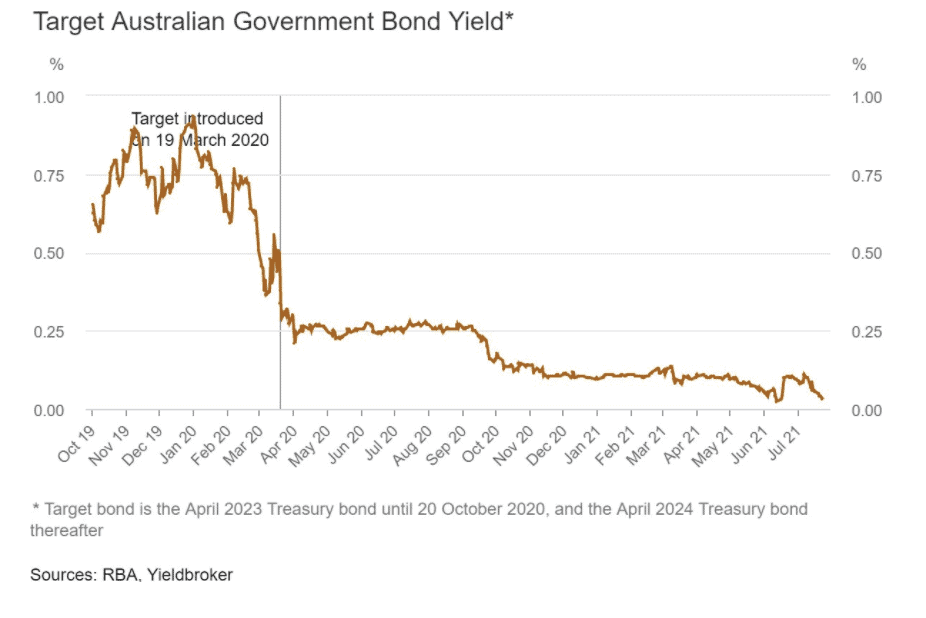

Indeed, on 3 November 2020, the Reserve announced a reduction of the yield target to around 0.1 per cent.

Plus, on 6 July 2021, it announced that the target would continue to apply to the then-current three-year Australian Government bond, which was the April 2024 bond.

How does it support the economy?

The purchase of government bonds will see the RBA receive regular interest payments – 0.1 per cent – for the life of the bond, with the investment amount repaid at maturity.

This means that at the end of the bond term, the government does have to repay the Reserve, which is essentially the same way it would occur if the bond was held by another entity.

Also, the Reserve if purchasing the bonds from the ‘secondary market’ in auctions three times a week.

This means that institutional investors, such as banks (both foreign and local), buy bonds directly from the government, and then the Reserve will purchase them from these investors, according to Canstar.

In the Reserve’s most recent statement on monetary policy it said that the bond purchase program had been one of the factors underpinning the accommodative conditions necessary for economic recovery from the pandemic.

Given the high degree of uncertainty about the economic outlook, it was agreed that there should be flexibility to increase or reduce weekly bond purchases in the future.

This is the slow down of bond buying that I mentioned at the start of this blog.

Interesting, the Reserve also said that as economic outcomes had been materially better than expected and the outlook had improved, a reduction in weekly bond purchases from $5 billion to $4 billion was imminent – even with the current Sydney lockdown.

What does it mean for property and interest rates?

There has been plenty of conjecture lately about interest rates increasing much sooner than the 2024 timeframe that the central bank has indicated numerous times.

However, the Reserve remains committed to that time period.

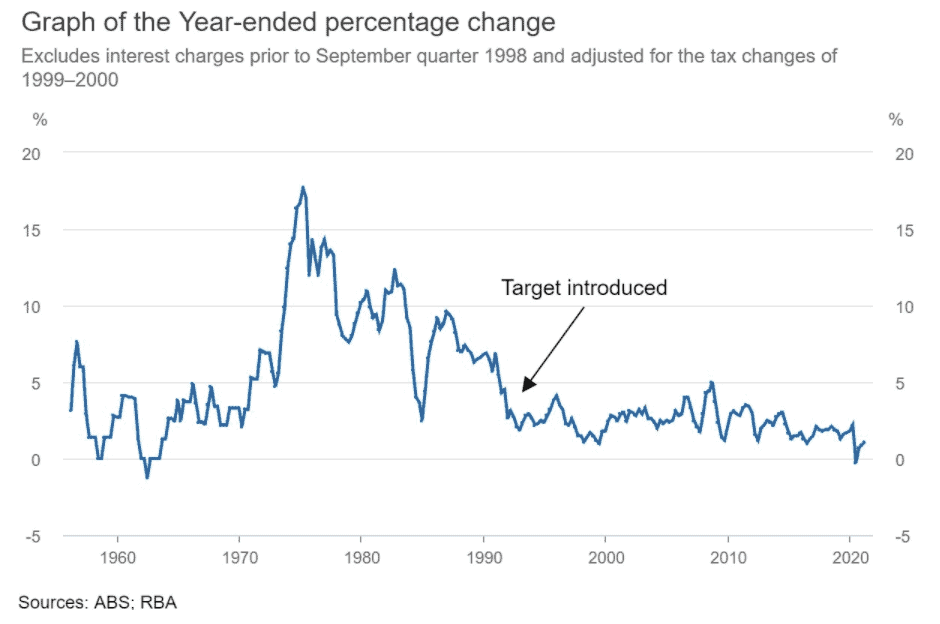

That’s because it wants to see inflation increase sustainability to between its two to three per cent target band before normalising monetary policy, including the removal of high levels of bond buying.

What this means in practice is that inflation not only needs to be within this target band, but it needs to have been there for a number of quarters before interest rates are lifted from their current record lows.

So, if anyone wants to know what is likely to happen with interest rates, they really should only listen to the monetary policy decision-makers themselves!

The Reserve also says it will not increase the cash rate until actual inflation is sustainably within that range – and its central scenario for the economy is that this condition will not be met before 2024.

Fundamentally, this means that the current and sustained level of highly supportive monetary policy is set to have a positive impact on property markets for a while yet.